Applicable Fraction Isn’t Just a Calculation – It Can Be an Unfixable Mistake

Low-Income Housing Tax Credit (LIHTC) deals don’t run in straight lines. Schedules move and the lease-up gets messy. Development has their written plan, site staff has an entirely different reality – and somewhere in the middle, everyone is trying to make sure that the entirety of their credits are earned.

Applicable fraction lies in the middle of this chaos and requires your full attention.

Many people see this as a math problem you can solve at the end, shifting different items until everything fits “just right.” But in practice, it’s something you either protect throughout the lease-up or slowly lose without realizing it.

Once it lands on the 8609, that’s it – the number is finished, never to be adjusted for the life of the credits. There just simply isn’t a clean-up phase later where everything can be balanced out.

Why This Rule Exists, and Why It Matters

The rule itself is simple: applicable fraction is the lesser of the unit fraction or the floor space fraction, calculated by building, NOT by project. The math itself may be simple, but the reason behind it is crucial to the ongoing integrity of affordable housing and the spirit behind the funding itself.

Without this calculation, affordable units can quietly drift toward the smallest, or least desirable, spaces. The consideration of floor space forces a level of fairness that doesn’t necessarily happen organically during development or leasing.

Every leasing decision affects your applicable fraction; each unit filled carries more weight in your calculations, so careful planning and tracking is crucial from day one.

Where Things Can Go Wrong

Most issues concerning the applicable fraction rarely come from a misunderstanding of the rule – they appear during normal operations. Lease-ups can move at an uncomfortably fast pace; designations are swapped between units because one tenant wants the 2nd floor two-bedroom unit instead of the 1st floor unit, but they exceed the AMI limit originally set for the units. These adjustments are noted, written down with all other crucial information throughout the process, so that someone can review and correct it later.

They usually don’t.

It’s absolutely noticed when underwriting assumptions and day-to-day site operations seem to drift apart into their own separate realities. Your Pro Forma looks clean and final, but that is because it involves paper, not people. Once occupied units are set, it’s not unusual to see that the Pro Forma was written for the perfect lease-up and never truly factored in the realities of what happens on site.

By the time monitoring or file reviews catch the change, it is already history written in stone and a permanent monetary loss.

“One Unit” Problem Is Not an Overstatement

Yes, it truly can come down to a single unit in the building.

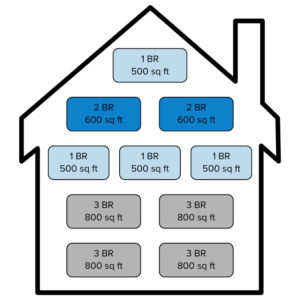

In the examples below, you can see how a building with 10 units can go from 100% applicable fraction to much less with just one misstep.

A simple building with 10 units and differing floor plans could be calculated differently based on number of units leased and square footage, even though the intention was for all units in the building to be considered 100% LIHTC funded.

Example 1: What You Are Looking For

Ideally, all units in the building will be rented to qualified households, and all units are occupied before the end of the tax year. In this case, the applicable fraction calculations are made:

- 10 LIHTC qualified units / 10 units – 100% Applicable Fraction

- 6400 sq ft occupied by LIHTC qualified units / 6400 sq ft total – 100% Applicable Fraction

Example 2: Market Rate Units

Buildings can be rented with the intention of having both LIHTC funded units and market rate units. When the focus is only on the number of units leased at the applicable rate, and size of units is not considered, credits can be easily lost.

As an example, if the building was to have 8 units designated as LIHTC funded, and 2 market rate units, it absolutely matters which units are designated as which. Consider the following:

- 2 market rate units are 3-bedroom units:

- 8 LIHTC units / 10 total units – 80% Applicable Fraction

- 4800 sq ft occupied by LIHTC qualified units / 6400 sq ft total – 75% Applicable Fraction

- 2 market rate units are 1-bedroom units:

- 8 LIHTC units / 10 total units – 80% Applicable Fraction

- 5400 sq ft occupied by LIHTC qualified units / 6400 sq ft total – 84% Applicable Fraction

Something as basic as the size of the units can move your applicable fraction from a planned 80% to 75%, ultimately decreasing the number of credits the building will earn – permanently.

Example 3: Delayed Lease-Up

Development teams never hesitate to remind lease-up staff that units must be occupied before the end of the tax year to earn the credits expected in the project. But, what if that Certificate of Occupancy isn’t received until the end of October, and all units were not able to be leased by the end of the tax year?

- 1 1BR and 1 2BR are not leased by year end:

- 8 LIHTC occupied units / 10 total units – 80% Applicable Fraction

- 5300 sq ft occupied by LIHTC qualified units / 6400 sq ft total – 82.8% Applicable Fraction

When this situation occurs on a project that was slated for 100% credit earnings based on the anticipated applicable fraction, the building financial outlook is permanently crippled– there is no way to fix these numbers later.

Any of these situations may not seem like a big deal – just another day and another lease-up and the difficulties that come with it. And someone, somewhere, must be tracking these small changes to ensure full credit earnings… right?

Applicable fraction is often labeled a compliance responsibility, but it rarely starts there. Development builds financial expectations around it, investors watch it closely as the 8609 approaches, and leasing and management staff influence the figure every single day, usually without considering the crucial math behind their decisions. When these groups stop talking to each other regularly, the impact becomes real.

Diligence and Monitoring Can Be Rewarded

For projects that follow their Pro Forma, that make it through lease-up without any major issues and tracked meticulously every move to ensure a 100% applicable fraction – you may be eligible to complete Alternate (or Self) Certifications after initial occupancy.

Projects will always need to verify and confirm with their State Housing Agency, as some may require the request of a waiver to perform Alternate Certifications. Site staff will not be required to complete full income and asset certifications of their qualified tenants and will reduce the overall administrative burden of ongoing compliance. The work and diligence up front rewards management over the credit life of the project.

Applicable fraction does not, however, reward good intentions. A decision may be made to switch a designation of a unit because it met a family need or allowed a resident to have mobility features needed for quality of life – but without appropriate communications and proper tracking of the big picture, these accommodations may be detrimental to the financial health of the project.

Track designations early. Ask more questions than you think you need to. And assume that small decisions will matter more than they look like in the moment – because sometimes they really do.

Owners and Management Agents should be well trained in understanding the rules and regulations of the affordable housing programs pertaining to their properties as they relate to maintaining compliance. MLCM offers consulting services and training regarding various affordable housing programs. For more information on these services, don’t hesitate to contact us.

The information presented in this article is intended solely for informational purposes and should not be construed as consulting advice from M&L Compliance Management LLC.

About the Author

Becky joined MLCM in September 2025 as a Housing Compliance Consultant. She has extensive experience in the affordable housing industry, beginning her career in property management as both an on-site manager and resident services coor… Read more